What's Possible? Financial Independence for Everyone

- Blair Hoover

- Mar 11, 2023

- 3 min read

Updated: Jul 21

When I was just a few years out of university and trying to find my way in the world, I did a quick calculation of my expenses and tried to figure out how much I would need to save to ensure I had 30+ years worth of money for retirement. It was immediately evident to me that I would never be able to save enough to support myself for a prolonged period. I would never have full financial independence.

This was the mid 2000's, I was making just a little above US minimum wage. Paying my student loans, credit card debt, rent and car payment used up almost all of my income. I was barely able to make ends meet each month. Saving anything was a challenge. Saving enough to make a difference in my future looked impossible.

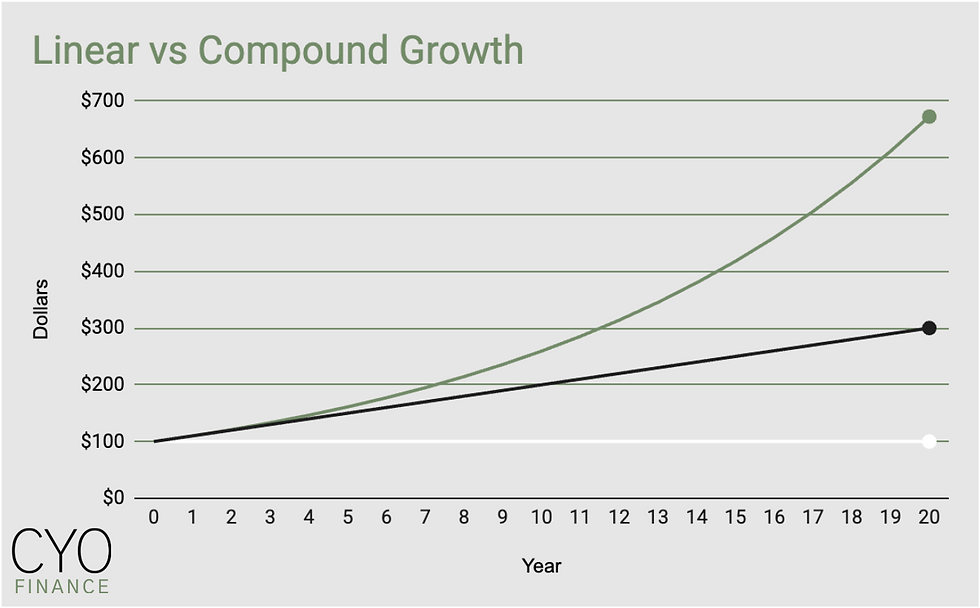

What I didn't know then was the power of compound interest.

Compound interest works against you if you're in debt. It's why it's so hard to get out of debt, because the balance grows exponentially.

But compound interest can work in your favor. Essentially, compound interest is earning interest on interest.

Oversimplified example: If you invest $100 and earn 10% interest on it annually, after one year you will have $110. The original $100 plus $10 (the ten percent interest). If you reinvest that $10, the following year you earn 10% on that too. So your interest earnings will go up to $11 the second year, for a total of $121 after the second year. Each year your interest earnings will increase because you're earning interest on more money.

Money grows faster the longer it's invested.

So, how does this change what's possible?

Because we know that on average, the total stock market has increased by about 10% per year over the past 100 years, we can make the assumption that it will, on average, continue to do so.

If we are able to invest in the entire stock market (diversification) then, over time, our investments will grow. (Note that this is not true in the short term due to volatility)

So we don't have to save all of the money that we'll need in retirement, some of it will come from compound interest. The longer the timeline, the more work compounding will do for you.

AND we don't actually need to save 30+ years of expenses, we only need about 25 times our annual expenses at retirement, and that should last forever.* This is known as the 4% rule. We use it to estimate our financial independence (FI) number (the amount of money you need invested in order to support yourself only from the interest earned in that investment).

FI Number = Annual Expenses X 25

The amount of money you need to save is lower than you might think, and your money can grow. So it's actually easier to get financial independence (aka retirement) than you might have guessed (if you were me at 26).

You can accelerate the time it takes to get to your FI number by increasing your earnings and/or decreasing your expenses. This is why expense tracking is so beneficial.

If you already know your annual income and annual expenses you can figure out how long it would take you to get to FI using Networthify's Retirement Calculator. (Assuming you invest your savings in the whole stock market.)

Mr Money Mustache wrote this excellent post about how quickly you can get to your FI number. The main idea is encapsulated in this table:

Knowing what's possible gives you enough information to make initial financial goals, It keeps you from thinking it's impossible, and it also set realistic expectations. Now that you know the basics, it's time to put it in action! If you find you're having trouble getting started, sign up for a free intro call and I'll give you your next steps.

If I can FI, so can you. I did it the messy way. You don't have to be perfect to find financial freedom.

*Note that there is nuance to the 4% rule, and early retirees may sometimes need additional support (lower withdrawal rate, flexible spending, additional income sources) in order for the money to last forever in bad market conditions. However a 4% withdrawal rate is still likely to last forever and a useful planning tool, and for traditional retirement it's still reliable even in bad market conditions.

Comments